We don’t dispute.

We demand.

90-day money-back guarantee. If we delete nothing from your reports in 90 days, you pay nothing. Every dollar back.

Federal-grade credit restoration for working families nationwide. Our team of credit experts hits the creditor and the federal regulator direct, in week one, and we don’t stop until the line on your report is clean.

•All 50 states

•$499 flat · no monthly drip

•First round inside 30 days

•FCRA & FDCPA grounded

•90-day money-back guarantee

K

Kali’s assistant

Reviewing your file

i. The fileEvery line of paperwork, audited.

i. The fileEvery line of paperwork, audited.

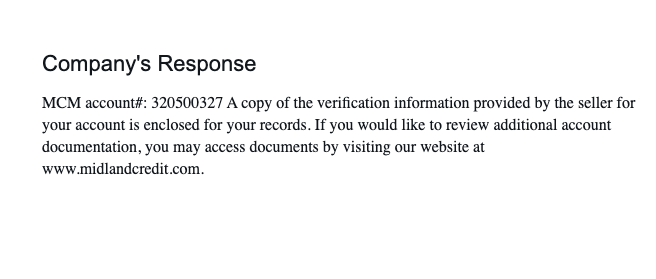

ii. The lettersDemands and federal complaints, filed.

ii. The lettersDemands and federal complaints, filed.

iii. The deskWorked by our team, week after week.

iii. The deskWorked by our team, week after week.